7. November 2008

30 Danish proposals for EU simplification

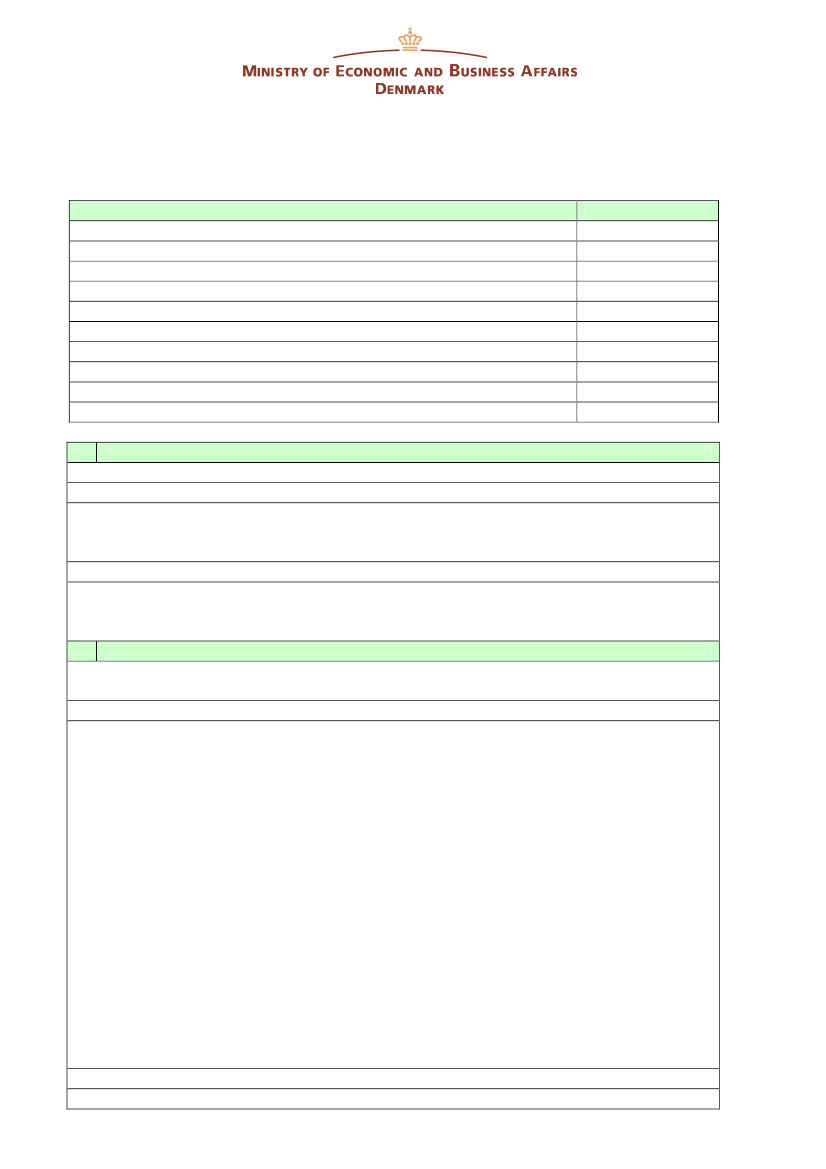

Area of the proposal

Environment

Company Law

Company Law – accountancy

Food safety

Fisheries

Agriculture

Statistics

Financial

Maritime

Total

No of proposals

4

5

2

2

3

3

4

5

2

30

1 Environment

European Waste Shipment Regulation 1013/2006 EC.

Description of simplification proposal

Digitalisation – to develop a standardised interface for exchange of information and documents

listed in article 26 of the Regulation for all Member States instead of the current paper based

administrative procedures.

Reason for simplification

DK proposes that a joint electronic interface for the exchange of data for electronic transposi-

tion between European Member States is developed. This could reduce the administrative bur-

dens for both companies and authorities in the Member States.

2 Environment

Directive 2000/76/EC of the European Parliament and of the Council of 4 December 2000 on

the Incineration of Waste.

Description of simplification proposal

DK wish to put forward two proposals regarding the directive on waste incineration:

1) Exemption from the requirements of continuous measurements on waste incineration plants

and waste co-incineration plants with a nominal capacity of less than 6 tonnes per hour.

The authority may decide not to require continuous measurements for NO

x,

total dust, TOC,

HCl, HF and SO

2

and require periodic measurements or no measurements when the waste

fractions are homogenous and well defined – typically arising in the industry.

2) DK proposes the sampling time for dioxins and furans is proposed to be 30 minutes to 8

hours like for heavy metals. This will make the measurement of dioxin a lot more cost ef-

fective and will not have a negative effect on quality.

This will require a revision of the WI directive (Article 11, para 4 and annex II, para II 2.2 and

annex V, para (d))

The revisions are preferred to be accomplished through an independent fast track procedure in

relation to the waste incineration directive or alternatively in connection to the current revision

of the IPPC-directive. The last option will require a revision of the recast of the IPPC (Annex

VI, part 6, para 2 and annex VI, part 3, para 1.4 and annex VI, part 4, para 4.2).

Reason for simplification

Today the authority can decide not to require continuous measurements for HCl, HF and SO

2

.